As far as I know, these have never been published on the web like this as I experienced some problem in finding them when doing some bond pricing project.

Closed-form formula:

A single arithmetic formula obtained to simplify an infinite sum in a general formula. The general formula of bond duration and bond convexity cannot be said closed-form as there is an infinite sum over the different time periods. Using a closed-form formula, a bond’s duration or convexity can be calculated at any point in its life time.

Bond duration closed-form formula (Richard Klotz):

C = coupon payment per period (half-year)

P = present value (price)

i = discount rate per period (half-year)

a = fraction of a period remaining until next coupon payment

m = number of coupon dates until maturity

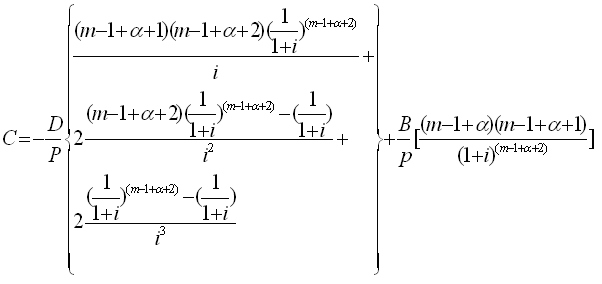

Bond convexity closed-form formula (Blake and Orszag):

D = coupon payment per period

P = present value (price)

B = face value

i = discount rate per period (half-year)

a = fraction of a period remaining until next coupon payment

m = number of coupon dates until maturity

Download the sample Excel spreadsheet >>>

password protected, email anymatters@gmail.com for permission

No comments:

Post a Comment